POSITION YOURSELF - HOW TO BENEFIT FROM A CRASH

Have you ever wondered why, after every major market crash, a handful of elite investors suddenly become much, much richer? It’s not luck. It’s because they follow a specific, mechanical pattern—the "Three Trades"—that turns panic into profit. This pattern is unfolding now, suggesting the next big global correction could be near (late 2025/early 2026). Here is the plan, translated into simple action steps ... for an Indian investor

FEATURED

I am an investor, an hobbyist investor. I have been following the news avidly and was fascinated by the prediction of a crash and what Not to do, and yes, what we can do to survive it. I have been investing over the years and have had a fair amount of success, not to mention, failures too. My knowledge has come from reading, cautious practices and most importantly, learning, figuring it out, and evolving my approach. This article is NOT for professionals, it's an informational blog for folks like me who are navigating investments on their own.

I spent some time reading and reviewing multiple sources to prepare myself in the event of an 'alleged' crash. I share my findings in this article specifically focused on an Indian investor. You must know by now, this is related to the enormous US debt and its logical consequences, leading to prominent doubt's about USA's ability to pay-back and various theories about how the USA is trying to mitigate the situation it's in. I am unsure about when the market will crash, or, if it will be a minor / major correction. I do know that the financial landscape is not in an ideal plane. It will correct.

So, let's proceed. Ravi is an Indian investor, with some experience and is still learning to navigate the financial landscape. He has had some successes with failures too.

Meet Ravi: An Indian Investor

Let's look at Ravi, a prudent Indian investor with a total fund base of ₹2.5 Lakhs spread across:

₹1.25 Lakh in Direct Equities (Stocks)

₹1.00 Lakh in Equity Mutual Funds (MFs)

₹0.25 Lakh in Gold ETFs

Ravi’s goal is to protect his ₹2.5 Lakhs from a major crash or correction and use the crisis to multiply his wealth. What can Ravi do?

The Three Trades: Ravi’s Crash Strategy

The core idea is to shift from a high-risk portfolio to a defensive position, creating (cash) for the alleged fire sale.

Trade 1: Raise Cash (The Defense Shield 🛡️)

This is the most crucial step: moving money out of risky assets (stocks) and Mutual funds and into safe assets (cash) before the crash. Ravi can move them into a Liquid Funds These funds are a type of low-risk debt mutual fund in India that invest in short-term money market assets with a maturity of up to 91 days. They allow investors to access their money quickly within 24 hours. These type of funds give an annualized return of approximately 7-8%, which is typically higher than a savings account's 2-5%. This is an estimate, as actual returns will vary based on market conditions and the specific fund's performance.

Ravi’s Action:

Ravi needs a minimum of ₹75,000.

He decides to sell ₹25,000 worth of his most volatile stocks (from his ₹1.25 L equity portfolio) and redeem ₹50,000 from his Mutual Funds (MFs).

He shifts the ₹75,000 into a Liquid Fund, making his portfolio 30% safer, giving him a better interest rate and allows him to keep this pool of money to buy later.

Trade 2: Accumulate Gold (The Purchasing Power Protector 💰)

When global panic hits, governments often print huge amounts of money to save the economy,. Due to excess cash in the economy, the currency devalues, meaning the cash in your hand buys less. In such situations, Gold acts as a hedge or a buffer protecting us against this loss of money value or devaluation. Ravi should protect his money from losing value and the best way is to invest in Gold. Ideally, he should invest in SGB's [Sovereign Gold Bond (SGB)]. An SGB is digital gold issued by the government. You don't get a physical coin, but you get a certificate proving ownership. Best of all? It pays you a small amount of interest every year, and it’s very tax-efficient

Ravi’s Action:

Ravi already holds ₹25,000 in Gold ETFs, which is a good start.

He uses ₹15,000 of his liquid fund cash to buy a new tranche of Sovereign Gold Bonds or Gold ETF's

Result: His gold exposure increases to ₹40,000, protecting him from currency collapse and inflation.

Trade 3: Bet on Volatility (The Crash Insurance 📈)

Take a bet. Bet that a market correction will happen. As with bets, we will have to put in a certain amount of money. If the bet fails, we will lose the money. But, if you are right, you make a lot of money. This is the aggressive play that turns a small investment into a massive profit when the market drops. It's called a "Put Option". A put option is basically like buying insurance for your stock! 🛡️

Here's the lowdown: When you buy a put option, you're get the right to sell a stock at a specific, agreed-upon price (which is called the strike price) before a certain date hits (the expiry. Think of it like this:

You pay up a small fee, called the premium, for this right.

If the stock price goes below your strike price, you can either use your option to sell the stock at that higher strike price, or just sell the option itself for a sweet profit.

Imagine this:

You own 100 shares of "Company X," trading at ₹100 / share. You're feeling a little nervous about a potential loss.

Here's where you take the Insurance: You buy a put option with a ₹100 strike price that expires in a month. This "insurance" costs you a premium of ₹5 per share (so, ₹500 total for 100 shares). This is like betting that the stock price will fall below 100.

Now, when Company X's stock dips to ₹80 per share, you would have notionally lost Rs 2000/- (20*100).

Since You have the option now - Thanks to your put option, you can still sell your shares for ₹100—@ the strike price—even though everyone else is only getting ₹80! That's a ₹20 per share win over the market.

You pocket ₹20 per share (₹100 sale price - ₹80 market price) minus the ₹5 premium you paid for the policy. That leaves you with a clean net profit of ₹15 per share (a whopping ₹1,500 total!)

In a worst case Situation - If the stock price stays above ₹100 by the time the option expires, no worries! Your put option simply expires worthless. You only lose the Rs 500/- (₹5 premium * 100 shares) that you paid. That ₹5 was your peace of mind, the small cost for having "insurance" for that month!

Ravi’s Action:

Ravi allocates a small, expendable amount—₹5,000—to buy long-dated (6-9 months expiry) Put Options on the Nifty 50 index

Result: This small ₹5,000 is his insurance premium. If the market rises, he loses ₹5,000 (his insurance cost). If the Nifty crashes or corrects by 30%, that ₹5,000 could turn into ₹25,000 - ₹50,000 in profit, adding significantly to his buying power.

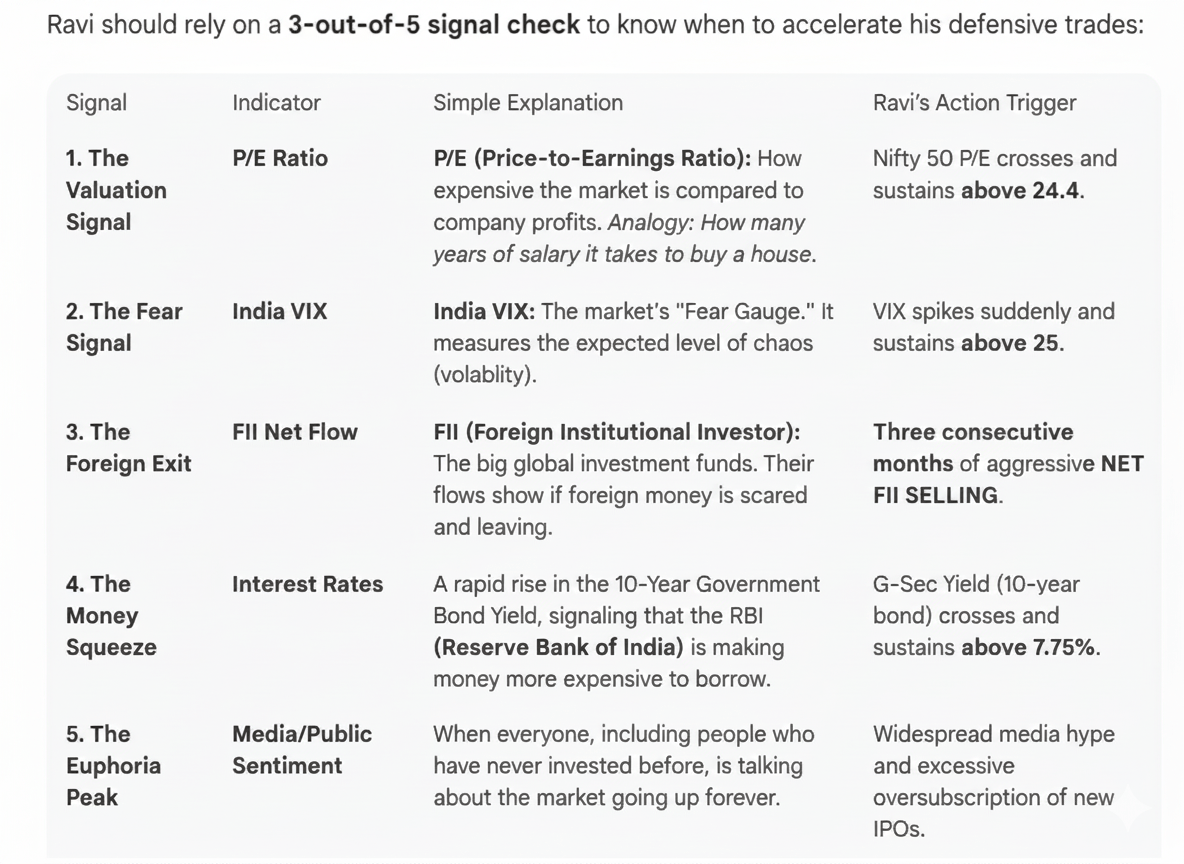

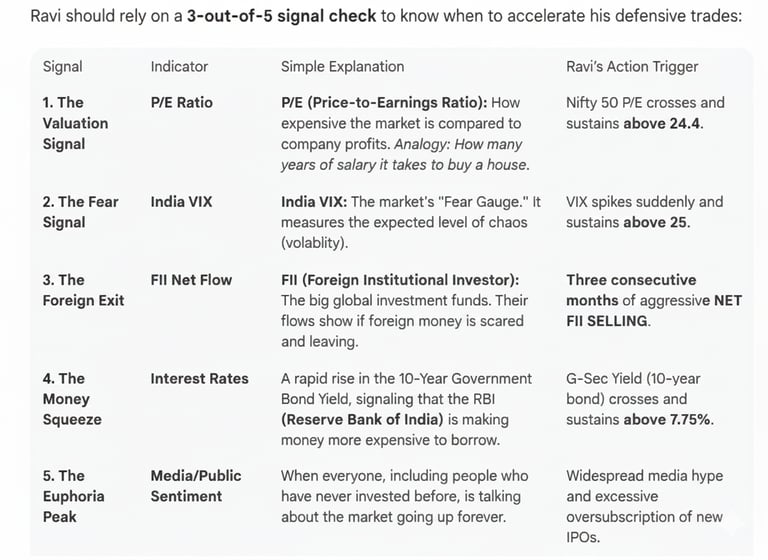

When to Start these trades. Understanding the Indian Market Signals

Remember, you may have to accept that you will miss the final 5-10% gain when you sell ahead of a crash. You will have to rely on a convergence of indicators, not just one.

Disclaimer:

This article is for informational and educational purposes only and is not financial advice. Investing in the stock market involves risks, and derivative products like options carry significant risk of capital loss. Always consult with a qualified financial advisor before making any investment decisions.

The Valuation Signal (The Macro Warning)

What to watch: The Nifty 50 Price-to-Earnings (P/E) Ratio. This tells you how "expensive" the market is compared to company profits.

The Trap: A very high P/E (like the COVID-era 40) often meant earnings had collapsed, not that prices were ridiculously high. Today, a P/E of ~22.6 is near the historical upper boundary for India.

Your Trigger: When the Nifty 50 P/E crosses and sustains above 24.5 for a few weeks, it's a strong red flag that the market is becoming overvalued. This is your cue to accelerate Trade 1 (cash conversion) and consider Trade 3 (Put Options).

The Fear Signal (The Panic Button)

What to watch: The India VIX (Volatility Index), often called the "Fear Gauge." This measures how much panic and volatility the market expects.

Your Trigger: The VIX usually sits below 15 when things are calm. A sudden spike and sustained level above 25 indicates that institutional panic has begun. This is the moment your Put Options (Trade 3) bought earlier will start making serious money.

The Fund Flow Signal (The Foreign Exodus)

What to watch: FII (Foreign Institutional Investor) Net Flows. Look for monthly data on major financial news sites.

Your Trigger: Three consecutive months of NET FII SELLING (foreign money actively leaving the Indian market), especially if local DII (Domestic Institutional Investor) buying starts to slow down, confirms that global "risk-off" sentiment is severely impacting India. This is a powerful signal to ramp up your cash position (Trade 1).

The Interest Rate Signal (The Economic Squeeze)

What to watch: The India 10-Year Government Bond Yield.

Your Trigger: A rapid and sustained rise in this yield above 7.75% signals that the Reserve Bank of India (RBI) might be tightening money supply aggressively, or the market is very nervous. High interest rates choke corporate growth and consumer spending, often preceding an economic slowdown.

The News/Sentiment Signal (The Euphoria Peak)

What to watch: Pay attention to general financial media headlines and everyday conversations.

Your Trigger: When analysts are confidently predicting Nifty 30,000+ in the near future, when even non-finance friends are giving stock tips, and when every new IPO is massively oversubscribed—this indicates extreme euphoria and a lack of caution. Historically, this is a dangerous time to be fully invested.

The Final Step: The Fourth Trade (The Fire Sale)

With the start of the crash when the market enters maximum panic (VIX spikes high), equities, mutual funds and other assets prices start a downward trend due to immense selling pressure and that too at significantly discounted prices, Ravi does the opposite of everyone else. He calmly uses his:

₹75,000 Cash (from Trade 1)

₹25,000+ Profit (from Trade 3)

Total Buying Power: ₹1 Lakh

...to buy stocks in his "shopping list" (quality, reliable companies) that are now trading at a 40-50% discount. This is how he converts a crisis into generational wealth.

Impact of Geopolitical Headwinds & India’s Resilience.

Once the crash starts, every country will be affected by the headwind. India is the only economy growing at a very good rate. India will be impacted. There will be a correction. However, due to the Indian economic progress and its strength, it's anticipated that India will be able to recover faster than any other country.

The Immediate Impact: A crash in the US or Europe will cause FII selling in India and a temporary sharp drop in the Nifty. No market is immune to global panic.

The Indian Advantage: Our strong Domestic Institutional Investor (DII) buying (investments from local mutual funds/SIPs) acts as a powerful safety net, cushioning the fall. India's economy is also driven by domestic consumption, making it more resilient to global export slowdowns. While we fall, we bounce back faster.

Don't Cash Out Too Early: The Psychology of Patience

The fear of missing out on the market's final climb is real. To manage this:

Accept Missing the Peak: No one, not even the billionaires, perfectly times the market top. The goal is to preserve capital and have liquid funds, not to extract every last rupee from the peak.

Your "Insurance" Helps: Knowing you have a small bet on the market falling (Trade 3 - Put Options) helps emotionally. If the market continues to rise, you lose only that small, pre-defined amount, but you participated in the ride. This makes it easier to hold your cash (Trade 1) patiently.

By understanding these signals and applying the "Three Trades" strategy, an Indian investor with a ₹2.5 Lakh portfolio can strategically protect their assets and position themselves for significant gains during the inevitable next market correction